Rigetti Computing (RGTI) Stock Analysis 2026: The High-Risk Quantum Play That Could 10Xs

1. INTRODUCTION – THE MOST ASYMMETRIC BET IN QUANTUM COMPUTING

The race to build the world’s most powerful quantum computer is no longer theoretical, it is now a high-stakes industrial competition involving governments, Big Tech, and a new class of deep-tech disruptors. At the center of this race sits Rigetti Computing, one of the few publicly traded companies attempting to build scalable quantum hardware from the ground up.

What makes Rigetti particularly compelling, and controversial is not just its ambition, but its approach. Unlike companies that specialize in only one layer of the quantum stack, Rigetti has chosen to control everything: chip design, fabrication, control systems, and cloud delivery. This full-stack strategy, combined with its bold bet on chiplet-based quantum architecture, positions it as one of the most technically differentiated players in the industry.

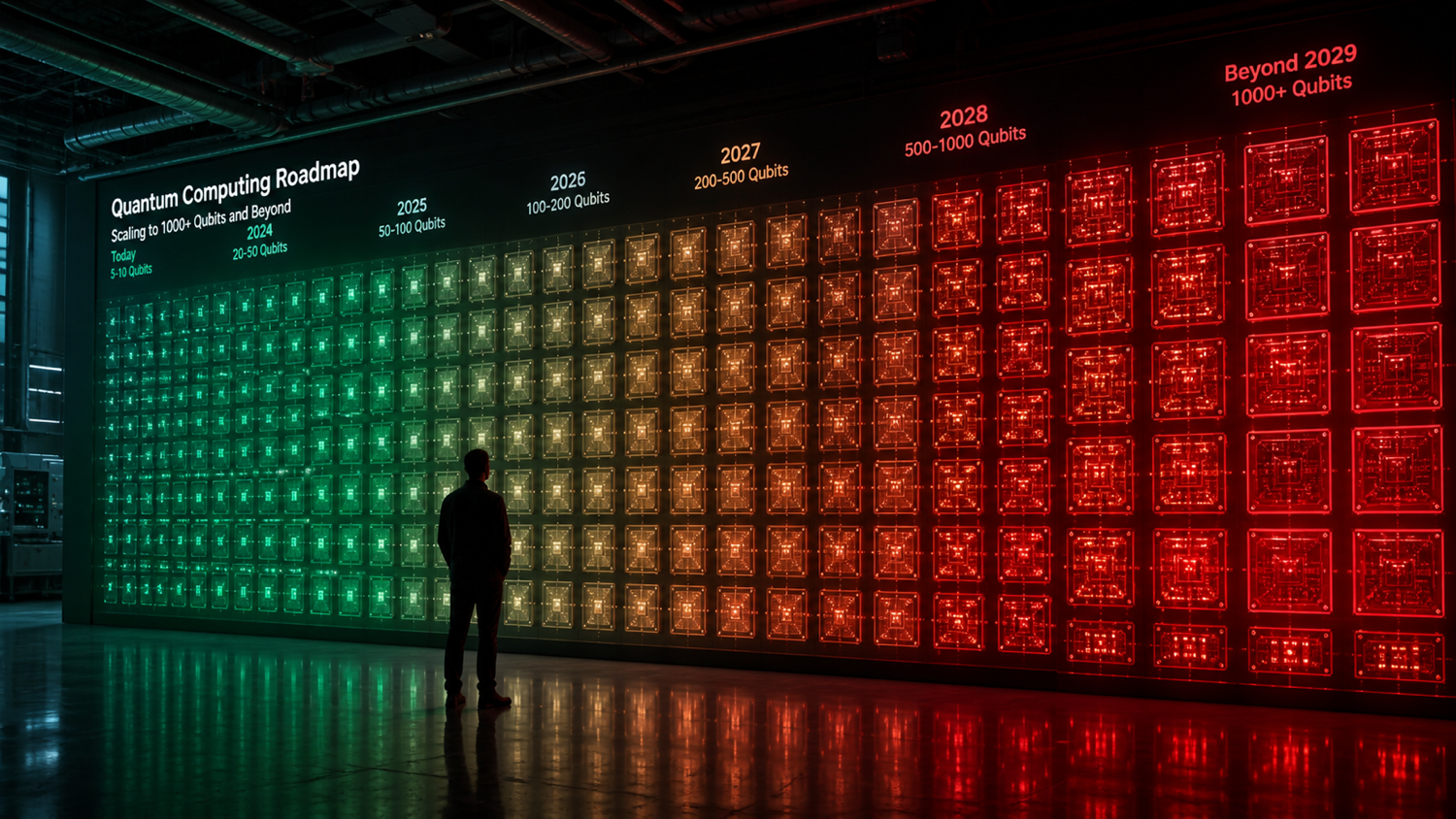

The timing of this story is critical. The quantum computing industry has entered what many analysts consider an inflection point. Hardware is no longer confined to laboratories. Systems are now being shipped, cloud access is expanding, and government contracts are increasingly translating into real revenue pipelines. In April 2026, Rigetti reached a major milestone by launching its 108-qubit Cepheus system, making it broadly accessible through its cloud platform and partner ecosystems.

Yet, for all its technological progress, Rigetti remains one of the most polarizing stocks in the market. With 2025 revenue of just $7.1 million against a multi-billion-dollar valuation, investors are not buying the present, they are betting on a future where quantum computing becomes a foundational layer of global computation.

This creates a uniquely asymmetric setup:

- If Rigetti succeeds → it could become a foundational infrastructure company

- If it fails → the valuation has little fundamental support

This article provides a complete, investor-grade deep dive into Rigetti’s technology, business model, financials, risks, and long-term investment outlook, so you can determine whether this is a speculative gamble or a generational opportunity.

2. COMPANY OVERVIEW: A FULL-STACK QUANTUM PIONEER

Founded in 2013 in Berkeley, California, Rigetti Computing was established by Chad Rigetti, a former IBM quantum researcher who believed that quantum computing could scale faster if one company controlled the entire development stack. This philosophy remains the core of Rigetti’s identity today.

At its core, Rigetti is not just building quantum computers, it is building a complete quantum computing platform. This includes superconducting quantum processors, proprietary control systems, and cloud-based access through its Quantum Cloud Services (QCS). The company’s vertically integrated model allows it to iterate rapidly across hardware and software layers without relying on external manufacturing or tooling dependencies.

Rigetti’s product ecosystem is built around several key offerings. Its Cepheus quantum processors, ranging from 36 to 108 qubits, represent its flagship systems designed for both cloud and on-premises deployment. Complementing this is the Novera QPU, a smaller 9-qubit system targeted at research institutions that already possess cryogenic infrastructure. These systems are delivered either through direct hardware sales or accessed via cloud platforms such as Amazon Braket.

The company’s customer base reflects the early-stage nature of the industry. Rather than mass-market adoption, demand is currently concentrated among government agencies, national laboratories, and academic institutions. Recent contracts, including an $8.4 million system order from India’s C-DAC and a quantum networking project with the U.S. Air Force, highlight the strategic importance of quantum computing at the national level.

Geographically, Rigetti is expanding beyond the United States, with deployments in the UK and planned expansion into Asia. Its commitment to invest $100 million in the UK quantum ecosystem signals both ambition and confidence in long-term global demand.

Ultimately, Rigetti’s positioning is clear: it is not trying to be a niche player, it is attempting to become a foundational infrastructure provider for the quantum era.

3. TECHNOLOGY & CORE INNOVATION: THE CHIPLET THESIS

To understand Rigetti, you must understand its central technological bet: chiplet-based quantum computing.

Most quantum companies face a fundamental scaling problem. As quantum processors grow larger, they become exponentially harder to manufacture and maintain due to issues like decoherence, crosstalk, and fabrication yield. Traditional approaches attempt to build larger monolithic chips, but this quickly runs into physical and engineering limits.

Rigetti’s solution is conceptually simple but technically ambitious: instead of building one large quantum chip, it builds smaller, high-performance chiplets and connects them together into larger systems.

This architecture has already been demonstrated in its product lineup. The 36-qubit system is composed of four smaller chiplets, while the 108-qubit system integrates twelve chiplets into a single modular processor.

The analogy to classical computing is powerful. Just as companies like AMD overcame scaling limits by adopting chiplet-based CPU designs, Rigetti is attempting to apply the same principle to quantum hardware. If successful, this approach could unlock a faster and more scalable path to large-scale quantum systems.

Beyond architecture, Rigetti’s technology stack is built on superconducting transmon qubits, one of the most mature quantum computing modalities. These qubits offer extremely fast gate speeds, measured in nanoseconds, which provide a significant computational advantage in certain workloads.

Recent technical progress further strengthens the narrative. In March 2026, Rigetti demonstrated 99.9% two-qubit gate fidelity at 28-nanosecond speeds on a prototype platform, marking a significant improvement in performance metrics.

However, the technology is not without risks. Scaling chiplets introduces new complexity in calibration and interconnect stability. Maintaining coherence across larger systems becomes increasingly difficult, and the company has yet to demonstrate fault-tolerant quantum computing, which remains the ultimate goal of the industry.

Still, the roadmap is aggressive. Rigetti is targeting 1,000+ qubit systems by 2027, a milestone that, if achieved, would place it among the leaders in quantum hardware scaling.

4. BUSINESS MODEL & REVENUE ENGINE: EARLY, LUMPY, BUT STRATEGIC

Rigetti’s business model reflects the realities of a pre-commercial deep-tech industry. Revenue is generated through a combination of cloud access, hardware sales, and government contracts, each with very different characteristics.

The most scalable component is Quantum Cloud Services (QCS), which allows developers and enterprises to access Rigetti’s quantum processors remotely. While this model has long-term potential, it currently contributes only a small portion of total revenue due to limited commercial demand.

Hardware sales, on the other hand, represent larger but highly irregular revenue events. Systems such as the Novera and Cepheus processors are sold to research institutions and government agencies, often resulting in multi-million-dollar contracts that do not recur consistently.

Government funding remains a critical pillar. Contracts with organizations such as DARPA and the U.S. Air Force not only provide revenue but also validate the company’s technology. The recent AFRL quantum networking project is a prime example of how government partnerships are shaping the early quantum economy.

This hybrid model leads to lumpy and unpredictable revenue patterns, which can make financial analysis challenging. However, it also reflects a broader truth: quantum computing is still in its infrastructure-building phase, not its mass commercialization phase.

Over time, the key transition investors should watch is the shift from:

- Government-driven revenue → Enterprise-driven revenue

- Hardware sales → Recurring cloud usage

That transition, if it happens, will define Rigetti’s long-term valuation.

5. FINANCIAL ANALYSIS: STRONG BALANCE SHEET, WEAK REVENUE BASE

Rigetti’s financial profile is a study in contrasts.

On one hand, the company has a very strong balance sheet, ending 2025 with approximately $589.8 million in cash and investments, largely due to capital raises. This provides a multi-year runway, allowing the company to continue investing heavily in research and development without immediate financing pressure.

On the other hand, its revenue remains extremely small. Full-year 2025 revenue came in at just $7.1 million, representing a decline from the previous year. Quarterly revenue has remained relatively flat, fluctuating around $1.5–1.9 million with no consistent upward trend.

Losses are significant but expected for a company at this stage. Rigetti reported a GAAP net loss of $216.2 million in 2025, driven largely by R&D investment and non-cash accounting adjustments.

Looking forward, analyst expectations are highly optimistic. Revenue is projected to triple in 2026 to around $20–22 million, driven by system deliveries and contract execution. Longer-term forecasts suggest potential growth to over $100 million by 2028, though these projections are highly dependent on execution.

From a valuation perspective, Rigetti is still priced as a future technology leader rather than a current business. This makes the stock extremely sensitive to both positive and negative developments.

6. RISK ANALYSIS: WHERE THE THESIS CAN BREAK

Investing in Rigetti requires accepting a wide range of risks, many of which are structural rather than cyclical.

The most obvious risk is valuation disconnect. With revenue in the single-digit millions and a multi-billion-dollar market cap, the stock is entirely dependent on future expectations. Any delay in execution can lead to significant downside.

Technology risk is equally important. The chiplet approach, while promising, has not yet been proven at large scale. Challenges in coherence, error correction, and system stability could emerge as the company attempts to scale beyond 100 qubits.

Financial risk is also present. Although the current cash position is strong, continued losses and capital-intensive expansion, such as building new fabrication capacity, could eventually require additional funding, leading to shareholder dilution.

Finally, there is the broader industry risk. Quantum computing remains an uncertain field, with multiple competing approaches and no clear winner. It is entirely possible that a different technological pathway could ultimately dominate. Rigetti’s strong competitors include IonQ and D-Wave (QBTS)

7. INVESTMENT OUTLOOK: A HIGH-RISK, HIGH-CONVICTION PLAY

Rigetti is not a traditional investment, it is a long-duration technology bet.

The bull case is straightforward. If the company successfully scales its chiplet architecture and achieves meaningful quantum advantage, it could become a foundational player in a multi-hundred-billion-dollar industry. Revenue growth would accelerate, enterprise adoption would increase, and the current valuation could look conservative in hindsight.

The bear case is equally clear. If scaling proves more difficult than expected or if competitors achieve breakthroughs first, Rigetti could struggle to justify its valuation. In such a scenario, the stock could remain volatile or decline significantly.

The most realistic outcome lies somewhere in between. Progress will likely be incremental rather than exponential, with periodic breakthroughs followed by setbacks. Investors should expect volatility and be prepared for a long holding period.

FINAL VERDICT: IS RIGETTI A GENERATIONAL OPPORTUNITY OR A SPECULATIVE BET?

Rigetti Computing represents one of the most fascinating opportunities in modern technology investing.

It is a company attempting to solve one of the hardest engineering challenges ever undertaken, with a strategy that could either redefine computing, or fail under its own complexity.

For investors, the key is positioning:

- This is not a core portfolio holding

- This is a high-risk, high-upside allocation

- It requires patience, conviction, and tolerance for volatility

In the end, Rigetti is not just a stock, it is a bet on the future of computation itself.

❓ Frequently Asked Questions (FAQ)

What does Rigetti Computing do?

Rigetti Computing is a full-stack quantum hardware company that designs, builds, and operates superconducting quantum computers and provides cloud access through its QCS platform.

Is Rigetti (RGTI) a good investment in 2026?

Rigetti is a high-risk, high-reward investment dependent on scaling its chiplet architecture and achieving commercial adoption over the next few years.

What is Rigetti’s chiplet architecture?

Rigetti uses a modular chiplet approach, combining smaller quantum processors into larger systems to improve scalability and performance.

How does Rigetti make money?

Rigetti generates revenue from cloud access, hardware sales, and government R&D contracts.

What are the biggest risks of investing in Rigetti stock?

Risks include unproven technology, low revenue, high valuation, and strong competition in quantum computing.

What is Rigetti’s long-term goal?

Rigetti aims to build scalable quantum systems exceeding 1000 qubits and achieve quantum advantage for real-world applications.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any financial decisions. We are not responsible for any investment losses incurred based on the information provided in this article.