EOS Energy (EOSE) Stock Analysis 2025

Eos Energy Enterprises, Inc. (NASDAQ: EOSE) – A Cornerstone Analysis for Investors in Clean Energy Storage

Keywords: EOSE, EOSE Stock Analysis, Clean Energy Storage

(Note: this article is written for informational purposes and does not constitute investment advice.)

Introduction

In recent years, the powerful narrative around artificial intelligence and semiconductor chips has captured the imagination of investors worldwide. But as we look into the next frontier of major industrial and societal transformation, another theme is gaining traction: energy storage. The core challenge behind the transition to renewables (solar, wind, etc.) isn’t just generation, BUT it’s the ability to store electricity effectively so that supply can match demand in real time and over longer durations.

One company that sits squarely in this emerging opportunity is Eos Energy Enterprises (ticker: EOSE). Eos aims to tackle the grid-scale storage bottleneck with an alternative chemistry to lithium-ion batteries—one rooted in zinc and manganese, aqueous electrolytes, and heavy emphasis on utility-scale deployments rather than consumer gadgets. In this article, we’ll explore EOSE’s business model, its competitive moat, its recent financial performance, and the risks and potential challenges for investors.

For readers of a financial and AI-savvy investment blog, the parallel is compelling: just as AI required infrastructure (data centres, chips, memory) beyond the algorithm, the “energy revolution” requires storage infrastructure beyond generation. EOSE positions itself as a technology and infrastructure play in that bigger framework.

Business Model

What EOSE does

Eos Energy Enterprises develops, manufactures, and markets utility-scale battery energy storage systems (BESS) based on its proprietary zinc-based aqueous technology (branded Znyth™, Z3 modules) rather than the dominant lithium-ion chemistry.

Key elements:

- The battery modules store energy in a zinc deposition/aqueous electrolyte system.

- Eos promotes its systems for 3- to 12-hour duration applications, which is in the “mid-duration” storage category (longer than typical “short duration” lithium systems, but shorter than multi-day flow battery systems).

- The systems are targeted at utilities, commercial & industrial, and renewable energy integration use‐cases: e.g., grid stability, congestion management, outages, and pairing with renewables.

- Eose’s manufacturing is U.S.-based, materials (zinc, manganese, water, graphite, etc.) are claimed to be abundant/domestic, thereby reducing dependence on more volatile supply chains.

Revenue / Commercial Model

- Eos sells complete energy-storage systems (cells + modules + power electronics + packaging + controls). The “system” is more than just a battery “cell box”.

- The company is in early commercial deployment stage (versus pure R&D) and sells to large customers (utilities, developers).

- It has a pipeline of projects under contract or under development; revenue recognition tends to lag deployment or commissioning (i.e., signing contract → build → acceptance → revenue).

- The company leverages government support: for example, a U.S. Department of Energy (DOE) loan guarantee program to scale manufacturing.

Why the model appeals

- Storage is often called the “secret sauce” of the energy transition because renewable generation (solar, wind) is intermittent—without storage, a portion of generation cannot be used or relied upon.

- A system that can deliver safe, reliable, long-life storage (3-12 h or more) at utility scale is a significant value proposition.

- By using abundant and less geopolitically constrained materials (zinc and manganese) and focusing on U.S. manufacture, Eos aims to align with policy tailwinds (e.g., Inflation Reduction Act, domestic supply chains).

- As grid assets, these storage systems have long life spans and can be recurring revenue over decades (maintenance, services), making the business model akin to infrastructure.

Where Eos focuses

- Mid-duration grid storage (3 to 12 hour, intraday shifting) rather than ultra-short (seconds/minutes) or ultra-long (multi-day).

- Utility-grade customers (municipalities, grid operators) rather than just consumer or vehicle batteries.

- U.S. domestic manufacturing and supply chain as a strategic differentiator.

Manufacturing / Scaling

- Eos plans capacity expansions: from current lower volumes to targeting GWh-scale production over coming years to reach cost competitiveness. For example, the company has an 8 GWh annual production target by 2027 under its “AMAZE” program.

- The cost structure and economies of scale will be critical: battery systems are capital-intensive and require high throughput to bring margins into a healthy zone.

Eos Energy Moat & Competitive Positioning

Technology Differentiation

- Chemistry & Safety:

- Eos uses a zinc-based aqueous chemistry (not lithium-ion with flammable organic electrolytes). Water-based electrolyte → inherently non-combustible, reducing fire risk.

- This matters especially for utility-scale systems where safety, reliability, regulatory approval and insurance are big hurdles.

- The claim: simpler structure, fewer moving parts, no extensive HVAC/pumping system, long cycle life (6,000+ cycles, 20+ years) in harsh environments.

- Materials Advantage:

- Many lithium-ion systems require cobalt, nickel, graphite, etc., some of which have supply chain/price risks and are subject to battery raw material volatility.

- Eos aims to use zinc, manganese, titanium, graphite felt, plastic and water: materials that are abundant, less volatile, and largely U.S. sourced.

- Domestic sourcing and manufacturing helps align with U.S. clean energy policy incentives (tax credits, domestic content requirements).

System Approach:

- Eos doesn’t just provide “cells”; they provide integrated system (battery modules, containerized solution, controls, power electronics) optimized for utility use. This gives more “stickiness” and customer switching cost.

- Containerized, plug-and‐play or near-plug solutions mean faster deployment and lower complexity, which is a competitive advantage.

Market-Specific Moat

- Utility Use-Case: Large utilities are understandably conservative about new storage technologies, and they favour solutions that are reliable, safe and have long life. Eos’s emphasis on safety and longevity aligns with that.

- Policy & Supply Chain Alignment: With energy policy focused on “made in America”, domestic supply chains and secure manufacturing become important. Eos is well positioned to tap that.

- Early Adoption / Reference Projects: Eos has moved from lab to deployed systems (rather than purely speculative tech). Having real projects boosts credibility and helps sales.

For example: real‐world deployments of Znyth-based systems, utility‐scale units etc.

Cost / Life-Cycle Advantage

- If Eos can deliver long life (decades) with stable performance, their cost of ownership for a storage asset may be lower than alternatives (i.e., fewer replacements, lower maintenance). This can be attractive for utilities.

- Scaling manufacturing and cost reductions are essential, but if they get there, they can achieve a cost advantage.

Pipeline Strength

- The company reports a very large project pipeline (tens of billions of dollars) which, if converted, could underpin high‐growth. For example, one report mentions a commercial pipeline of ~$18.8 billion/77 GWh.

- Large backlog or multi-project potential gives potential for a virtuous growth loop.

Eos Energy Financial Performance & Recent Developments

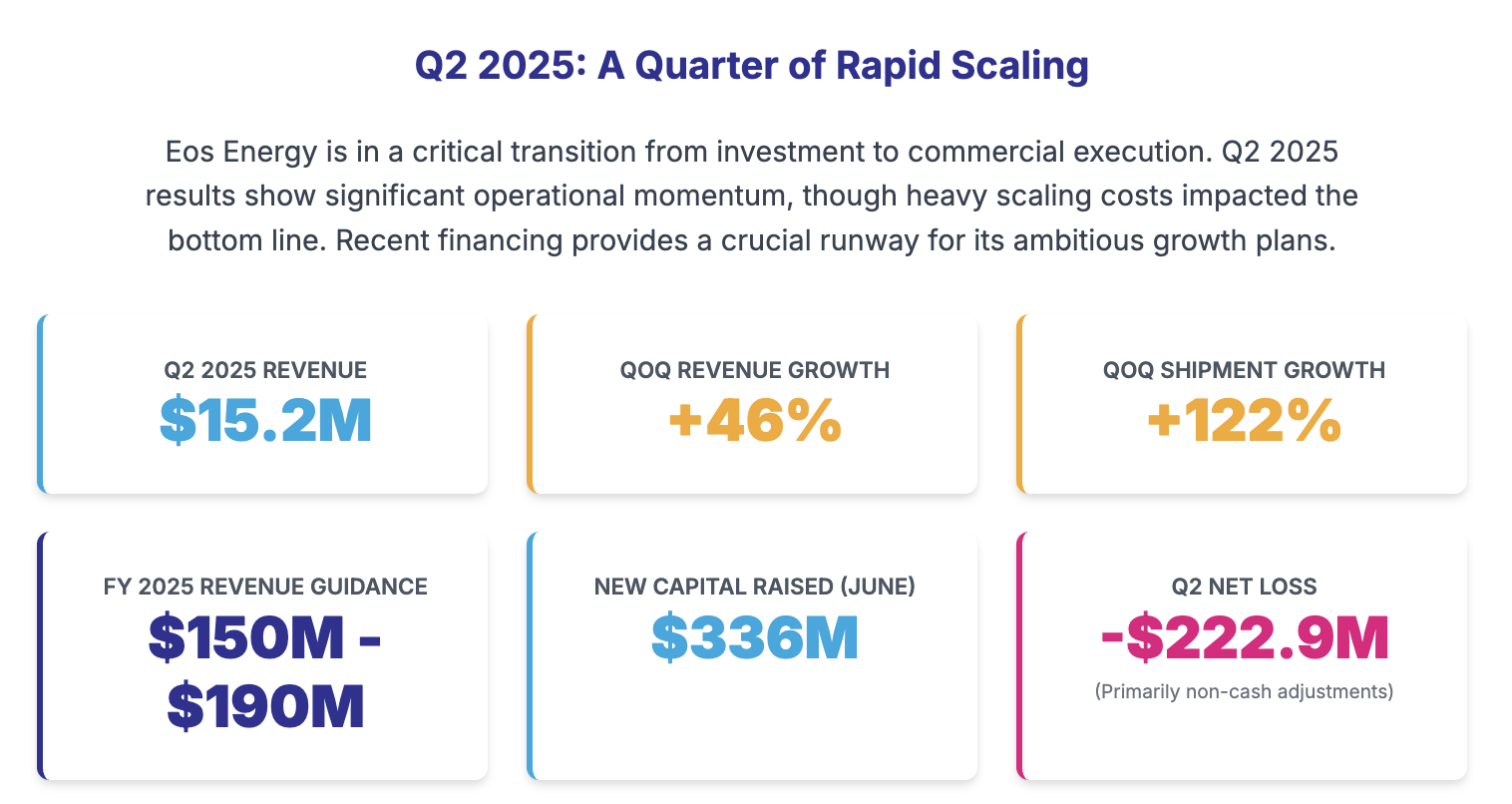

Recent Results – Q2 2025 Highlights

- Eos reported Q2 2025 revenue of USD $15.2 million.

- That represents a 46% increase over Q1 2025 and a ~17× year-over-year jump (compared to same quarter previous year) in some metrics.

- Shipments rose 122% quarter-over-quarter.

- The company reaffirmed its full-year 2025 revenue guidance in the range of US$150 million to US$190 million.

- Gross margin improved sequentially (~32% improvement) though still negative overall.

- However, the company posted a net loss of around US$222.9 million in Q2, driven by non-cash fair-value adjustments, debt-related charges, etc.

- Also, Eos closed a $336 million concurrent offering (common stock + convertible senior notes) in June 2025, strengthening its balance sheet.

- The company received a $22.7 million loan advance from the U.S. DOE’s Loan Programs Office (LPO) as part of a larger ~$303.5 million loan guarantee supporting its manufacturing capacity growth.

Historical / Baseline Financials

- For full year 2024, revenue was ~US$15.6 million (a small decline from 2023) and the company reported a large net loss (~US$964.2 million) according to one data source.

- The company is still in the investment / scale phase; cash burn is significant, and margins are negative.

Key Financial Metrics to Watch

- Revenue Growth: The ability to turn pipeline into bookings and bookings into revenue will signal traction.

- Gross Margin Improvement: As manufacturing scales, costs should come down; margin improvement is key to eventual profitability.

- Operating Cash Flow: As storage projects often have long lead times (contract → construction → commissioning → revenue), working capital/cash flow is a risk.

- Backlog / Pipeline Conversion: The size and convertibility of the project pipeline reflect future growth potential.

- Debt / Financing & Dilution: As a growth company with significant cash burn, how Eos finances growth and manages dilution (stock issuance, convertible notes) matters.

Recent Stock/Momentum Notes

- The company’s stock (EOSE) has been showing strong upward momentum recently (e.g., gap-ups in October 2025), with YTD returns reportedly 200%+.

- Analyst interest is picking up as the energy-storage thematic gains attention.

Market Trend & Industry Context

Why Energy Storage Is the Next Frontier

- The global energy transition (shift from fossil fuels → renewables + grid decarbonization) has a critical bottleneck: storage. Without effective storage, solar/wind cannot fully replace dispatchable power.

- Reports indicate that in the U.S., new storage capacity additions (10.4 GW in 2024) ranked second only to other power sources, pointing to accelerating growth in storage.

- Investors are shifting capital toward the “energy infrastructure” side of the energy revolution (which includes storage) rather than just generation or semiconductors. The narrative is: after AI and chips, storage might be the next explosive sector.

How EOSE Fits Into That Trend

- Eos is targeting grid-scale storage rather than EV or consumer batteries, a less crowded space with very high barriers to entry (scale, reliability, regulatory, financing).

- By focusing on non-lithium chemistry (zinc/manganese) and domestic manufacturing, Eos aligns with supply-chain resilience and policy incentives (e.g., the U.S. Inflation Reduction Act).

- Eos is moving from “story” to “deployment”: real systems, commercial customers, manufacturing scale up. This distinguishes it from many early-stage battery companies that are still in prototype phase.

Competitive Landscape & Positioning

- Lithium-ion battery systems dominate many storage applications (especially short-duration). But for mid-duration and long-duration storage, alternative chemistries (zinc, iron, flow batteries, etc.) are increasingly relevant.

- Eos competes not only on chemistry but system integration, reliability and cost over lifetime (not just initial capital cost).

- The moat is stronger in utility scale than in consumer markets because utility customers demand safety, long life, low maintenance and predictable cost of ownership.

Eos Energy Key Strengths

- Safety & reliability credentials: Non-flammable aqueous chemistry is a strong value-proposition for utilities.

- Materials/supply-chain advantage: Use of abundant, low-cost materials and domestic manufacture reduces geopolitical risk & potential cost volatility.

- Large pipeline: A significant project backlog and multi-billion-dollar commercial pipeline suggest future scale.

- Manufacturing scale/investment: Backing via DOE loan guarantee and strategic equity/convertible financing provides some runway for growth.

- Policy tailwinds: U.S. energy policy increasingly supportive of domestic battery manufacturing, grid resilience, and long-duration storage.

Eos Energy Challenges & Risks to Investors

Despite the clear opportunity, there are several material risks and challenges that investors must keep in mind.

- Scale / Cost Reduction Risk

- Battery manufacturing is a volume business: until scale is achieved, costs may remain high, margins thin or negative. Eos currently is low volume.

- If they cannot hit cost targets or manufacturing yield/performance targets, competitive pressure may squeeze margins.

- Execution risk: manufacturing ramp, quality assurance, module reliability, supply-chain issues, installation and commissioning on schedule.

- Conversion of Pipeline to Revenue

- Having a large pipeline is positive, but pipeline → contract → build → commissioning → revenue is a long lead-time cycle. Delays can postpone revenue recognition and cash generation.

- Storage project financing, regulatory approvals, grid interconnection and utility procurement are all complex and may introduce delays.

- Cash Flow & Funding / Dilution Risk

- Eos is still operating at a loss, with heavy investment in manufacturing and project growth. Supporting growth and surviving until positive cash flow will require careful financial management.

- The company has raised capital via stock and convertible notes; further financing may dilute existing shareholders.

- Long project payback timelines may strain working capital.

- Competitive Pressure

- The storage battery market is increasingly competitive: lithium-ion incumbents are improving and cost-reducing; other alternative chemistries are emerging.

- Eos must continue to differentiate and defend its niche.

- Technology risk: if alternative chemistries (solid-state, advanced lithium, or next-gen flow batteries) leap ahead, Eos may face margin pressure or risk of obsolescence.

- Regulatory / Policy Risk

- Although policy tailwinds exist, changes in incentives, tariffs, or supply-chain subsidies could impact economics.

- Utility procurement cycles and regulatory approvals can be slow and uncertain.

- Project Execution Risk

- Large utility-scale deployment projects carry execution risk: system integration, commissioning, interconnection, performance over time, warranty support.

- If field performance falls short, reputational and financial risk (maintenance, warranty claims) rises.

- Valuation & Expectation Risk

- Given the large pipeline and growth aspirations, investor expectations may be high. If Eos fails to meet milestone timelines or cost targets, there may be sharp re-ratings.

- As noted in some analyses, the company continues to burn cash, and the transition to profitability may still be years away.

Investment Thesis & Outlook

In summary: Eos offers a compelling investment thesis for those willing to accept risk in pursuit of the storage-infrastructure growth theme.

Why it could work:

- The underlying secular shift to storage (and particularly long-/mid-duration grid storage) is strong.

- Eos’s differentiation (zinc/aquous chemistry, U.S. manufacturing, system-level focus) provides a credible niche in a large market.

- The company is moving beyond R&D to commercial deployment with revenue growth already showing quarter-over-quarter improvement.

- Policy and supply-chain tailwinds favour domestically manufactured battery solutions.

- If Eos hits its manufacturing cost targets, scales production, converts its pipeline, and improves margins, the upside could be significant.

Why caution is warranted:

- Execution risk and funding risk remain high.

- The company is not yet profitable, and margins remain negative.

- The gap between the large pipeline and actual revenue is non-trivial.

- Competitive and technology risk is real in the battery space.

- Valuation may already embed high growth expectations; any delay may lead to a correction.

Investor Profile

This stock is more suitable for:

- Investors with a long-term horizon (3-5+ years) who believe in the storage infrastructure thematic.

- Risk-tolerant investors comfortable with small/mid-cap emerging companies with volatile operating metrics.

- Those who are willing to monitor key execution milestones (scheduled manufacturing ramp, cost per kWh, margin improvement, backlog conversion).

- Less suited for investors seeking near-term profitability or low risk.

Key Milestones to Monitor

- Achievement of manufacturing capacity targets (for example, the company targets 2 GWh annualised production by end of 2025).

- Cost of storage (USD/kWh) improvements and gross-margin expansion.

- Conversion of large pipeline projects into booked orders, then to commercial revenue.

- Cash-flow improvement and reduction of cash burn.

- Project commissioning timelines and field performance of deployed systems.

- Financing / capital structure: further equity issuance or debt financing will affect dilution and cost of capital.

- Competitive announcements from rivals or new battery chemistries that threaten Eos’s value proposition.

Conclusion

For investors seeking exposure to the intersection of clean energy and infrastructure investment, Eos Energy Enterprises (EOSE) offers a fascinating case study. It stands at the confluence of several megatrends: the clean energy transition, grid-scale storage growth, domestic manufacturing, and alternative battery chemistries beyond lithium-ion.

The upside is compelling if Eos executes: a large total addressable market, a differentiated technology, strong policy tailwinds, and early signs of growth. The risk is real: the company remains in the early stage of scale up, with negative earnings, significant execution risk, and high expectations baked into the market.

In short: EOSE might be one of the more interesting pure-play grid-scale storage names in the U.S., but just as with any growth infrastructure stock, the road to profitability is long and full of execution hurdles. For investors willing to ride the volatility, it could offer asymmetric return potential; provided key milestones are hit.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any financial decisions. We are not responsible for any investment losses incurred based on the information provided in this article.