Redwire (RDW) Stock Analysis 2026: Forget SpaceX – This Hidden Aerospace Stock Could Hit $20

But before you invest in Redwire, you must read this article to understand if Redwire is for you:

The modern space race has entered a new phase.

For the past decade, investor attention has been dominated by launch providers like SpaceX and ambitious visions of colonizing Mars. But as the industry matures, the real economic value is shifting away from rockets and toward infrastructure – the systems that enable sustained activity in orbit.

This transition mirrors historical industrial revolutions. Railroads were not the endgame of industrialization; they were the enabler. Likewise, rockets are not the endgame of space,they are simply the transportation layer.

At the center of this transformation sits Redwire Corporation, a company positioning itself as a critical supplier of mission-essential space infrastructure and defense technologies.

With accelerating demand from satellite constellations, national security programs, and in-space manufacturing, Redwire has quietly become one of the most compelling “picks-and-shovels” plays in the emerging $1 trillion space economy.

This article provides a comprehensive, fact-based deep dive into Redwire stock (RDW), evaluating its technology moat, financial trajectory, risks, and long-term investment potential.

Investment Thesis: A Leveraged Bet on the Industrialization of Space

Redwire’s core investment thesis is straightforward but powerful:

It is not betting on who wins the space race, it is selling the tools required for everyone to compete.

Unlike launch companies, Redwire operates across:

- Satellite power systems

- Avionics and sensors

- In-space manufacturing platforms

- Defense and drone technologies

This diversified exposure creates a platform-level advantage, allowing the company to benefit from industry-wide growth rather than single-player success.

The strategic positioning becomes even more compelling when viewed through the lens of macro trends:

- Falling launch costs (driven by reusable rockets)

- Explosion of satellite constellations (Starlink, Kuiper)

- Rising geopolitical demand for space-based defense systems

- Emergence of commercial space stations and manufacturing

As orbital activity increases, demand for infrastructure scales exponentially, and Redwire sits directly in that value chain.

Business Model Evolution: From R&D Contractor to Scalable Manufacturer

Historically, Redwire operated as a collection of niche aerospace firms delivering non-recurring engineering (NRE) solutions, custom, project-based work with limited scalability.

However, the company is undergoing a critical transformation.

By 2025–2026, Redwire has shifted toward:

- Standardized product lines

- Repeatable manufacturing

- Production-scale contracts

This transition is already visible in its financial trajectory.

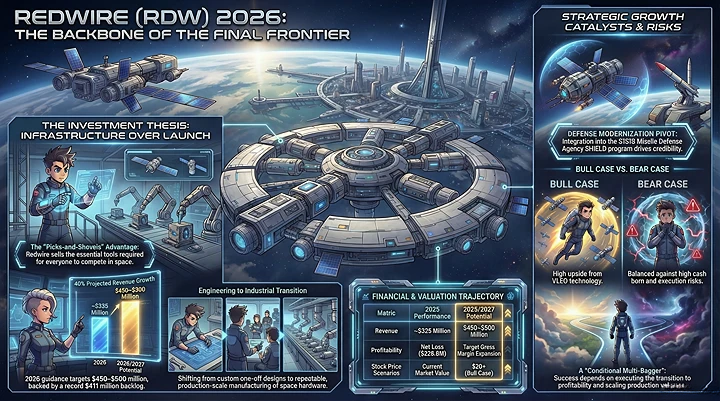

- 2025 revenue: ~$335 million

- 2026 guidance: $450–$500 million (≈40% growth)

- Record backlog: ~$411 million

This shift from development to production is the single most important driver of future margin expansion.

In essence, Redwire is moving from:

“Engineering company” → “Industrial platform”

Technology Deep Dive: Building the Backbone of Orbit

ROSA Solar Arrays: The Power Layer of Space

At the core of Redwire’s technological moat is its Roll-Out Solar Array (ROSA) platform.

Traditional solar arrays:

- Heavy

- Mechanically complex

- Prone to deployment failure

ROSA solves these constraints through flexible, rollable structures that:

- Reduce launch mass

- Improve reliability

- Increase power density

These systems are already deployed in:

- International Space Station upgrades

- NASA missions

- Commercial satellites

This is critical because in aerospace:

Flight heritage = trust = contracts

Once a component is proven in orbit, it becomes extremely difficult to displace.

VLEO Opportunity: A New Orbital Frontier

Very Low Earth Orbit (VLEO) represents one of the most strategically important emerging domains in space.

Operating closer to Earth enables:

- Higher resolution imaging

- Faster communication latency

- Enhanced defense capabilities

However, atmospheric drag makes traditional satellites unsustainable in this region.

Redwire’s solution, air-breathing propulsion systems, aims to fundamentally change this equation.

If successful, this technology could:

- Enable persistent surveillance satellites

- Unlock new defense markets

- Create a new category of orbital infrastructure

This is not a guaranteed outcome, but if validated, it represents asymmetric upside.

In-Space Manufacturing: The Long-Term Optionality Layer

Beyond hardware, Redwire is investing in microgravity manufacturing, including:

- Pharmaceutical crystal development

- Bioprinting technologies

- Advanced materials engineering

Recent developments include continued NASA-backed funding for microgravity drug development programs .

While still early-stage, this segment introduces:

- High-margin potential

- Non-government revenue streams

- Long-duration growth optionality

This is the kind of “call option” that can significantly re-rate a company over time.

Defense Pivot: The Most Important Strategic Shift

One of the most significant developments in Redwire’s story is its expansion into defense.

The company has:

- Integrated drone capabilities (via acquisitions)

- Aligned operations toward national security markets

- Reorganized its structure in 2026 to accelerate growth

This pivot is already delivering tangible results.

Key 2026 Catalyst:

Redwire was selected for the $151 billion Missile Defense Agency SHIELD program

While this is an IDIQ contract (not guaranteed revenue), it signals:

- Strong government alignment

- Increased credibility

- Access to large-scale defense budgets

Additionally, geopolitical dynamics are accelerating demand for:

- Drones

- Space-based intelligence systems

- Multi-domain defense integration

This positions Redwire at the intersection of two megatrends:

👉 Space commercialization

👉 Defense modernization

Financial Analysis: High Growth, But Not Yet Profitable

Redwire’s financial profile reflects a company in transition.

The financial profile of Redwire Corporation reflects a company in the midst of a critical transformation, from a fragmented, acquisition-driven aerospace roll-up into a scalable, production-oriented space infrastructure platform. This transitional phase is characterized by a compelling combination of strong top-line growth and near-term profitability pressure, a dynamic that investors must carefully interpret rather than evaluate at face value.

From a growth perspective, Redwire is demonstrating momentum that stands out even within the broader aerospace and defense sector. The company is guiding for approximately 40% year-over-year revenue growth into 2026, supported by a steadily expanding backlog and increasing demand across both its civil space and defense segments. This backlog provides a degree of forward revenue visibility, reducing uncertainty compared to earlier stages of its lifecycle. Importantly, the company’s growing exposure to defense-related programs, particularly in areas such as multi-domain operations and national security infrastructure, introduces a more stable and recurring revenue base, which could help smooth out the historically “lumpy” nature of aerospace contracts over time.

However, this strong revenue expansion has not yet translated into profitability, and that is where the financial story becomes more nuanced. Redwire reported a net loss of approximately $226.6 million in 2025, alongside negative EBITDA and compressed operating margins. At first glance, these figures may raise concerns about the sustainability of the business model. But a deeper analysis suggests that much of this weakness is transitional rather than structural. A significant portion of the losses can be attributed to one-time and non-recurring (NRE) factors, including goodwill impairments, acquisition-related expenses, and equity-based compensation. In addition, the company is still absorbing the costs associated with integrating prior acquisitions and building out its manufacturing footprint.

Another key driver of margin pressure lies in the legacy mix of development-heavy contracts. Historically, Redwire generated a large share of its revenue from custom engineering programs, which tend to carry lower margins and higher execution risk due to cost overruns and “estimate-at-completion” adjustments. As these programs mature and phase out, they are gradually being replaced by more standardized, production-scale offerings, particularly in areas such as solar arrays, avionics, and defense systems. This shift is essential because manufacturing scale, not engineering services, is where operating leverage begins to emerge.

Looking ahead, the investment case hinges on whether Redwire can successfully execute this transition. Management and external analysts have indicated that margins could improve materially as production volumes increase and the revenue mix tilts further toward repeatable products. In fact, some projections suggest that gross margins could potentially expand significantly, potentially even doubling in 2026 under favorable conditions. While this may appear optimistic, it is directionally consistent with the company’s strategic pivot toward industrialization and cost efficiency.

Ultimately, Redwire’s financials should not be evaluated through the lens of a mature aerospace contractor. Instead, they are better understood as those of an emerging platform company investing aggressively ahead of a potential inflection point. The current period of losses reflects front-loaded investments in scale, capability, and market positioning. If execution aligns with expectations, these investments could translate into meaningful margin expansion and operating leverage over the next several years. However, until that inflection is clearly visible in reported earnings, investors should expect continued volatility and remain focused on leading indicators such as backlog growth, contract wins, and improvements in gross margin trends.

Market Opportunity: The $1 Trillion Space Economy

The global space economy is projected to exceed $1 trillion by the 2030s.

Key growth drivers include:

- Satellite constellations (Starlink, Kuiper)

- Defense spending and militarization of space

- Commercial space stations

- Data demand driven by AI and connectivity

Redwire’s positioning allows it to benefit from all four simultaneously.

Unlike single-product companies, it operates across multiple layers of the ecosystem, creating resilience and scalability.

Competitive Positioning: Infrastructure vs Launch

Redwire competes with both legacy defense giants and emerging space companies.

Key competitors include:

- Lockheed Martin

- Northrop Grumman

- Rocket Lab

However, its differentiation lies in:

- Component-level specialization

- Proven flight heritage

- Vertical integration across systems

Most importantly:

Redwire is not competing directly with these companies, it is embedding itself within their supply chains.

Risks: What Could Go Wrong?

No high-growth aerospace company is without meaningful risks, and Redwire Corporation is no exception. While the long-term narrative around space infrastructure and defense modernization is compelling, investors must carefully evaluate several structural and execution-related challenges that could materially impact the company’s trajectory.

The most immediate concern is cash burn and capital intensity. Redwire remains in a transitional phase, investing heavily in scaling manufacturing capabilities, integrating acquisitions, and advancing next-generation technologies such as VLEO platforms and in-space manufacturing. These initiatives require substantial upfront capital, and the company has historically generated negative free cash flow. If the path to profitability takes longer than expected, Redwire may need to raise additional capital through equity issuance or debt financing. This introduces the risk of shareholder dilution, particularly if capital is raised during periods of stock price weakness.

Equally important is execution risk, which is often underestimated in aerospace and defense businesses. Transitioning from a research and development-heavy model to a production-scale manufacturing platform is operationally complex. It requires not only engineering excellence but also supply chain optimization, quality control, and cost discipline. Any delays, cost overruns, or technical failures, especially in mission-critical systems, could erode margins and damage Redwire’s credibility with key customers such as government agencies and prime contractors.

Another critical factor is contract uncertainty, particularly given Redwire’s reliance on government-related revenue streams. A significant portion of its backlog consists of IDIQ (Indefinite Delivery, Indefinite Quantity) contracts, which provide a framework for future work but do not guarantee actual revenue realization. Funding for these contracts is often subject to political processes, budget approvals, and shifting defense priorities. As a result, even awarded contracts may experience delays, reductions, or cancellations, creating unpredictability in revenue recognition and cash flow timing.

Investors must also be prepared for stock price volatility, as Redwire exhibits characteristics typical of emerging growth companies. The stock tends to have a high beta, with sharp price movements driven by news flow, contract announcements, or broader sentiment toward space and defense equities. This volatility can be amplified by relatively low institutional ownership and the presence of legacy shareholders gradually exiting their positions. For long-term investors, this creates both opportunity and risk, but it requires a strong tolerance for short-term fluctuations.

Finally, competitive pressure remains a structural overhang. While Redwire operates in a specialized niche, it ultimately competes within an ecosystem dominated by large, well-capitalized defense primes such as Lockheed Martin and Northrop Grumman. These incumbents possess significant resources and, in some cases, the capability to internalize functions that companies like Redwire currently provide. Over time, this could compress margins or limit market share expansion if Redwire fails to maintain its technological edge and cost competitiveness.

Taken together, these risks do not invalidate the long-term investment thesis, but they do highlight that Redwire is best understood as a high-risk, execution-dependent growth story. Investors should approach the opportunity with a clear awareness that while the upside potential is substantial, the path to realizing that value is neither linear nor guaranteed.

Valuation: Is Redwire Undervalued?

Because Redwire is not yet profitable, investors rely on Price-to-Sales (P/S) multiples.

Current context:

- Market cap: ~$2.3 billion

- Revenue (2026E): ~$450–500M

Valuation Scenarios:

- Conservative: $7–$12

- Base case: $12–$17

- Bull case: $20+

Recent analyst sentiment is turning positive, with upgrades suggesting meaningful upside potential .

Key Catalysts (2026–2027)

Several developments could drive re-rating:

- Defense contract execution (SHIELD program)

- Margin expansion from production scaling

- Continued backlog growth

- Success in VLEO technologies

- Broader sector momentum (potential IPO of SpaceX)

Each of these represents a step toward institutional validation.

Final Verdict: A High-Risk, High-Conviction Infrastructure Play

Redwire is not a mature, stable company.

⚖️ Redwire Stock: Risk vs Reward Framework (2026)

Understanding Redwire Corporation requires viewing it through a dual-lens framework:

👉 This is not a “safe compounder”

👉 It is a high-upside, execution-dependent growth play

🟢 The Bull Case (Why Bulls Are Interested)

1. Backbone of the Space Economy

Redwire is not competing in launches, it is supplying the infrastructure powering satellites, defense systems, and future orbital platforms. As space activity scales, demand for its components scales alongside it.

2. High-Growth Revenue Trajectory

With ~40% projected revenue growth into 2026, Redwire is operating at a growth rate rarely seen in traditional aerospace companies.

3. Defense Tailwinds Are Accelerating

Rising geopolitical tensions are driving increased spending in:

- Space-based intelligence

- Drone systems

- Multi-domain warfare

This directly benefits Redwire’s expanding defense segment.

4. Transition to Scalable Manufacturing

The shift from R&D-heavy contracts to repeatable production is expected to:

- Improve margins

- Increase revenue predictability

- Drive operating leverage

5. Asymmetric Upside Potential

If key technologies (like VLEO platforms or in-space manufacturing) succeed, Redwire could unlock entirely new markets.

👉 This is where the $20+ upside narrative comes from

🔴 The Bear Case (What Could Go Wrong)

1. Ongoing Cash Burn

Heavy investment in scaling operations may require additional funding, potentially leading to dilution if profitability is delayed.

2. Execution Complexity

Scaling aerospace manufacturing is non-trivial. Any misstep in production, quality, or delivery timelines could impact both margins and reputation.

3. Government Contract Dependency

A significant portion of revenue is tied to government programs, where:

- Budgets can shift

- Contracts can be delayed

- IDIQ awards are not guaranteed revenue

4. High Stock Volatility

Redwire behaves like a high-beta growth stock, meaning:

- Sharp price swings

- Sentiment-driven movements

- Potential short-term drawdowns

5. Competitive Pressure from Defense Giants

Large incumbents like Lockheed Martin and Northrop Grumman may internalize capabilities or outcompete on scale over time.

⚖️ Risk vs Reward Summary Table

| Factor | Risk Level | Upside Potential | Strategic Impact |

|---|---|---|---|

| Cash Flow | 🔴 High | 🟢 Medium | Key to survival |

| Execution | 🔴 High | 🟢 High | Determines scalability |

| Defense Exposure | 🟡 Medium | 🟢 High | Major growth driver |

| Technology (VLEO / ROSA) | 🟡 Medium | 🟢 Very High | Potential game-changer |

| Market Opportunity | 🟢 Low Risk | 🟢 Massive | $1T space economy tailwind |

| Valuation | 🟡 Medium | 🟢 High | Re-rating potential |

🧠 Investor Interpretation

This is the key takeaway:

👉 Redwire is a “conditional multi-bagger”

Meaning:

- If execution succeeds → outsized returns

- If execution fails → capital risk is real

🎯 Positioning Strategy (For Readers)

For investors, this typically fits into:

- High-risk growth allocation (5–10%)

- Not a core holding (yet)

- Requires long-term conviction + volatility tolerance

Bottom Line: The “Picks and Shovels” of the Final Frontier

If Tesla represents the electrification revolution, and SpaceX represents access to orbit,

Redwire represents the infrastructure that makes the entire system scalable.

For investors who believe in the long-term expansion of the space economy, Redwire offers a unique, high-upside opportunity to invest in the backbone of the next industrial revolution.

Frequently Asked Questions (FAQ)

Is Redwire Corporation a good stock to buy in 2026?

Redwire (RDW) is a high-growth space infrastructure company with significant long-term upside potential, particularly as the global space economy expands. However, it is not a low-risk investment. The company is still in a transition phase, with ongoing cash burn and execution risks. As such, Redwire is best suited for long-term investors who have a high risk tolerance and are comfortable with volatility in pursuit of outsized returns.

What does Redwire Corporation actually do?

Redwire provides critical infrastructure and technology solutions that enable space missions and defense operations. Its core offerings include solar arrays for satellites, avionics and sensors, in-space manufacturing platforms, and defense drone systems. By supplying these essential components, Redwire acts as a “picks-and-shovels” provider within the space economy, benefiting from overall industry growth rather than relying on a single segment like rocket launches.

Why is Redwire Corporation considered a space infrastructure stock?

Redwire is classified as a space infrastructure stock because it focuses on building the foundational technologies required for space operations. Instead of launching rockets, the company develops and manufactures the systems that power satellites, support orbital platforms, and enable long-term space activity. This positioning allows Redwire to benefit from increasing satellite deployments and the broader expansion of the space ecosystem.

Is Redwire Corporation profitable?

As of 2025, Redwire is not yet profitable. The company reported a net loss driven by heavy investments in scaling its operations, integrating acquisitions, and transitioning toward production-based revenue. While these investments are currently weighing on margins, profitability is expected to improve over time as the company increases manufacturing scale and shifts toward higher-margin, repeatable product lines.

What are the biggest risks of investing in Redwire Corporation?

The primary risks include ongoing cash burn, execution challenges in scaling aerospace manufacturing, and reliance on government contracts that may be delayed or uncertain. Additionally, the stock can be highly volatile, and competition from large defense contractors such as Lockheed Martin and Northrop Grumman could impact long-term growth. Investors should carefully weigh these risks before taking a position.

What is the price target for Redwire Corporation stock?

Based on current growth projections and industry valuation multiples, Redwire stock could reasonably trade in the $12 to $20+ range over the next few years. The upside depends heavily on successful execution, margin expansion, and continued growth in the space and defense sectors. While the potential is significant, investors should recognize that this outcome is not guaranteed and depends on multiple operational milestones being achieved.

More Questions Investors Are Asking About Redwire Stock

1. Is Redwire stock undervalued right now?

Redwire may be considered undervalued by some investors due to its high growth potential and exposure to the expanding space infrastructure market. However, its valuation depends heavily on execution and future profitability.

2. Who are Redwire’s main customers?

Redwire primarily serves government agencies and defense organizations, including NASA and the U.S. Department of Defense, along with commercial aerospace companies.

3. How does Redwire make money?

Redwire generates revenue by selling space infrastructure components, engineering services, and defense technologies to government and commercial clients.

4. What is Redwire’s competitive advantage?

Redwire’s key advantage lies in its flight-proven technologies, vertical integration, and role as a supplier of mission-critical space infrastructure.

5. Is Redwire a long-term investment?

Redwire is generally considered a long-term investment due to its exposure to the growing space economy, but it requires patience and tolerance for volatility

6. How does Redwire compare to other space stocks?

Compared to companies like Rocket Lab, Redwire focuses more on infrastructure rather than launch services, making it a complementary rather than direct competitor.

7. What industries benefit from Redwire’s technology?

Redwire’s technologies support multiple industries, including aerospace, defense, telecommunications, and biotechnology.

8. What is the future of the space infrastructure market?

The space infrastructure market is expected to grow significantly, driven by satellite expansion, defense needs, and commercial space development.

9. Does Redwire benefit from SpaceX growth?

Yes, as SpaceX increases launch frequency, it indirectly boosts demand for infrastructure components like those provided by Redwire.

10. What could drive Redwire stock higher?

Key drivers include successful contract execution, margin improvement, defense expansion, and overall growth in the space economy.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any financial decisions. We are not responsible for any investment losses incurred based on the information provided in this article.