Lumentum (LITE) Stock Analysis 2026: The Optical Backbone Quietly Powering the AI Revolution

The AI Optical Infrastructure Giant Entering a New Era

Artificial intelligence is no longer just a software story. It has become an infrastructure arms race. While investors have spent the past two years focusing heavily on GPU leaders like NVIDIA Corporation, a second layer of the AI ecosystem has quietly become equally important: the optical networking infrastructure that allows those GPUs to communicate with each other at extreme speed and scale. This is where Lumentum Holdings Inc. has emerged as one of the most strategically important companies in the entire AI supply chain.

Over the past twelve months, Lumentum’s stock has experienced one of the most explosive rallies in the technology sector. On May 11, 2026, the stock surged to new all-time highs above $1,050 after Nasdaq officially confirmed that Lumentum will join the Nasdaq-100 Index before the market opens on May 18, 2026.

The rally is not simply momentum-driven speculation. It reflects a major structural realization happening across Wall Street:

AI scaling increasingly depends on photonics and optical connectivity.

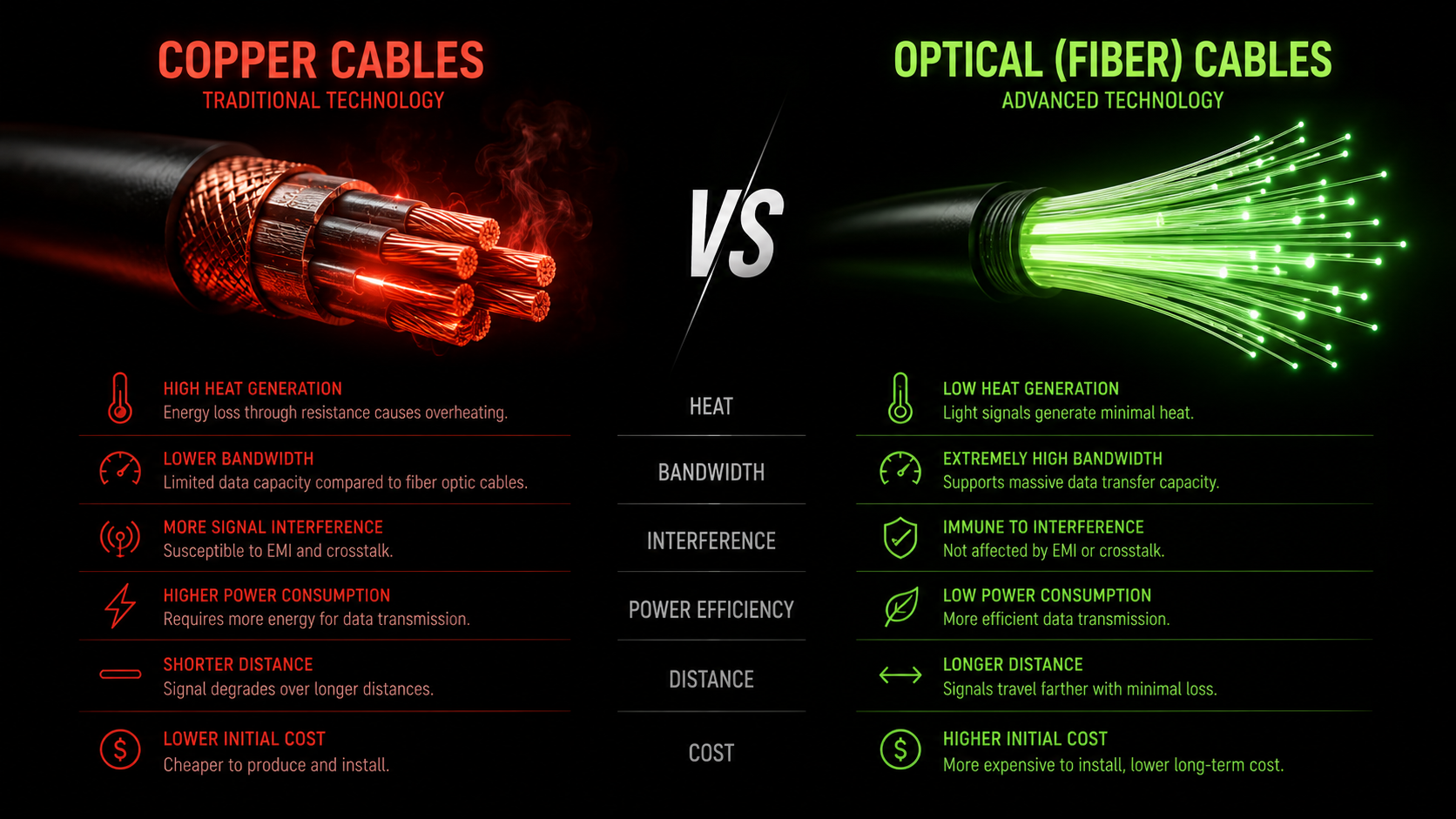

As AI clusters become larger and more computationally intensive, the bottleneck has shifted away from raw processing power toward data movement. Tens of thousands of GPUs inside hyperscale data centers must constantly exchange massive volumes of information during model training. Traditional copper-based electrical connections are reaching their physical limitations due to heat, signal degradation, and power inefficiencies. Optical networking has become the only viable path forward for next-generation AI infrastructure.

Lumentum sits directly at the center of this transformation.

The Hidden Infrastructure Behind AI

Most investors understand the importance of GPUs in artificial intelligence. Far fewer understand what happens between those GPUs.

Modern AI systems are highly distributed. Training large language models requires thousands of accelerators to synchronize data continuously. If communication latency rises even slightly, the entire training process slows down dramatically. In hyperscale environments, stalled synchronization can translate into enormous economic losses due to idle compute resources.

This problem becomes exponentially harder as clusters scale up or scale out from thousands of GPUs to potentially hundreds of thousands in the coming years.

Copper interconnects struggle at these speeds because high-frequency electrical signals degrade rapidly over distance. Heat dissipation also becomes increasingly problematic. This is why the industry is rapidly transitioning toward optical interconnects that transmit information using light instead of electricity.

That transition is creating a massive secular growth opportunity for photonics companies.

Unlike traditional networking vendors, Lumentum specializes in the actual optical engines powering these systems. The company designs and manufactures advanced laser technologies, optical components, and transceiver subsystems that serve as the foundation of high-speed AI networking.

In many ways, if NVIDIA provides the “brains” of AI infrastructure, Lumentum increasingly supplies the “nervous system.”

From Telecom Supplier to AI Infrastructure Leader

Lumentum’s transformation over the past several years has been remarkable.

The company was originally spun out of JDS Uniphase in 2015 and initially operated as a cyclical telecommunications equipment supplier. For years, investors largely viewed the business as tied to telecom carrier spending cycles and consumer sensing markets.

That perception has fundamentally changed.

Today, the overwhelming majority of Lumentum’s growth is tied directly to cloud networking and AI data center infrastructure. The company has successfully repositioned itself from a telecom component vendor into one of the core enablers of next-generation AI scaling.

This transition accelerated significantly following the company’s acquisition of Cloud Light Technology in late 2023. Before the acquisition, Lumentum primarily sold laser chips and optical components into the supply chain. After integrating Cloud Light’s advanced module packaging and assembly capabilities, the company gained the ability to deliver complete optical transceiver systems directly to hyperscale customers.

This vertical integration dramatically changed the company’s economics.

Instead of capturing only a small portion of the bill of materials, Lumentum can now participate in the much larger value pool associated with complete optical networking systems. The result has been a sharp increase in revenue growth, operating leverage, and strategic importance within the AI ecosystem.

Why Lumentum’s Technology Is So Difficult to Replicate

One of the most important aspects of the investment thesis is Lumentum’s technological moat.

The company’s core advantage lies in its expertise in Indium Phosphide (InP) semiconductor fabrication. Unlike traditional silicon semiconductors, compound semiconductors such as InP are extremely difficult to manufacture at scale. However, they are uniquely suited for high-performance optical communication because they can efficiently emit and modulate light.

This capability is essential for modern AI networking.

Lumentum manufactures several critical laser architectures used inside optical transceivers and co-packaged optical systems. Among the most important are Electro-Absorption Modulated Lasers (EMLs), which are used in ultra-high-speed 800G and 1.6T networking modules.

As data center bandwidth requirements increase, the industry is moving rapidly toward higher lane speeds.

The transition from 400G networking toward 800G and eventually 1.6T architectures requires increasingly sophisticated optical technologies. Lumentum has become a dominant supplier of the 200G-per-lane laser systems enabling these next-generation deployments.

This is not a market where new competitors can easily emerge.

Compound semiconductor manufacturing has enormous barriers to entry:

- Specialized wafer fabrication expertise

- Difficult yield optimization

- Reliability certification requirements

- Long qualification cycles with hyperscale customers

Once a component supplier becomes embedded inside hyperscale AI infrastructure, switching costs become extremely high because network reliability is mission-critical.

This creates a durable competitive moat.

The Co-Packaged Optics Revolution

The next major evolution in AI networking is likely to be Co-Packaged Optics (CPO).

Traditional networking systems place optical transceivers on the faceplate of networking switches. However, as switch bandwidth scales toward 51.2Tbps and beyond, electrical trace losses become increasingly severe.

CPO solves this problem by integrating optical engines directly next to switching ASICs.

The challenge is thermal management. High-performance lasers degrade under excessive heat, making it impractical to place the lasers directly beside the switch silicon.

This has created an entirely new market opportunity: External Light Sources (ELS).

Lumentum is emerging as one of the leading suppliers of these external laser systems, which feed optical engines inside co-packaged optical architectures. This could become one of the company’s largest long-term revenue drivers.

Management has repeatedly indicated that the scale-up optical networking market inside AI racks could eventually become several times larger than today’s traditional scale-out networking market.

If that thesis proves correct, Lumentum’s addressable market could expand dramatically over the next decade.

Financial Performance Has Entered Hypergrowth Territory

Lumentum’s recent financial results have fundamentally changed investor perception of the company.

In its latest quarterly earnings report released in May 2026, the company delivered record quarterly revenue of approximately $808 million, representing roughly 90% year-over-year growth. Non-GAAP EPS also significantly exceeded analyst expectations.

What matters most is not simply the top-line growth, but the operating leverage embedded within the business model.

As the product mix shifts toward high-speed optical systems and vertically integrated solutions, margins have expanded sharply. The company’s non-GAAP operating margin has climbed above 30%, a dramatic improvement compared to prior years when Lumentum operated as a lower-margin component supplier.

Investors are increasingly realizing that this may no longer be a cyclical hardware company.

Instead, Lumentum is beginning to resemble a strategic AI infrastructure platform with substantial long-term earnings power.

Management has outlined an ambitious long-term framework targeting:

- Multi-billion-dollar quarterly revenue potential

- Operating margins approaching 40%

- Significant free cash flow generation

While those targets remain aggressive, the current trajectory suggests the opportunity may be much larger than the market initially expected.

NVIDIA’s Strategic Investment Changed Everything

A major turning point for the company occurred when NVIDIA Corporation announced a strategic multi-billion-dollar partnership and investment into Lumentum.

The agreement included approximately $2 billion of strategic capital alongside long-term purchasing commitments tied to future AI infrastructure deployments.

This development carried enormous significance.

First, it validated Lumentum’s role as a critical supplier inside the AI ecosystem. Second, it provided the company with the financial resources needed to aggressively expand manufacturing capacity without materially stressing the balance sheet.

The company is now scaling production through multiple facilities, including expansion plans in Greensboro, North Carolina, designed to support future demand growth in advanced optical networking.

For investors, NVIDIA’s involvement effectively served as institutional confirmation that optical connectivity is becoming one of the most important constraints in AI scaling.

Nasdaq-100 and S&P 500 Inclusion Create Structural Demand

One of the most overlooked developments surrounding Lumentum in 2026 has been its rapid inclusion into major benchmark indexes.

The company joined the S&P 500 in March 2026 before Nasdaq subsequently confirmed that Lumentum will officially join the Nasdaq-100 on May 18, 2026, replacing CoStar Group.

This matters far more than many retail investors realize.

Inclusion into the Nasdaq-100 forces passive investment vehicles and ETFs tied to the index, particularly products linked to the QQQ ecosystem, to accumulate shares automatically. This creates structural buying pressure independent of short-term market sentiment.

The market reaction was immediate. On May 11, 2026, Lumentum shares surged approximately 17%, making it one of the top-performing stocks in the entire S&P 500 that day.

Importantly, the rally extended beyond Lumentum itself. Other optical networking and photonics companies such as Corning Incorporated and Coherent Corp also experienced major gains as investors increasingly recognized the broader AI optical infrastructure theme.

The combination of:

- explosive AI demand,

- rising institutional ownership,

- benchmark index inclusion,

- and constrained photonics supply chains

has created an unusually powerful momentum cycle around the stock.

Comparing Lumentum to Corning and Ciena

Investors often compare Lumentum with companies like Corning Incorporated or Ciena Corporation because all three are connected to the broader optical networking ecosystem.

However, their positions inside the stack are very different.

Corning primarily focuses on optical fiber and connectivity infrastructure. Ciena builds networking systems and optical transport equipment. Lumentum, by contrast, operates deeper within the photonics layer itself by manufacturing the lasers and optical engines enabling high-speed data transmission.

This distinction is important because the highest growth opportunities inside AI networking increasingly revolve around:

- optical transceivers,

- co-packaged optics,

- and advanced photonic integration.

These are precisely the areas where Lumentum has established leadership.

As AI clusters become denser and networking bottlenecks intensify, the value capture may increasingly migrate toward companies capable of solving the most difficult optical engineering problems.

Risks Investors Should Understand

Despite the powerful long-term thesis, Lumentum is not without substantial risks.

The company remains highly dependent on hyperscale AI spending cycles. Any slowdown in AI infrastructure investment from major cloud providers could materially impact growth expectations.

Valuation also remains a major concern. Following its extraordinary rally, Lumentum now trades at elevated earnings multiples that leave little room for execution mistakes. Investor expectations have become extremely aggressive, which increases volatility following earnings reports.

Supply chain constraints represent another important challenge. The company has acknowledged ongoing shortages in certain optical components and substrates, which may temporarily limit its ability to fully satisfy demand.

Competition is also intensifying. Companies such as Broadcom Inc., Marvell Technology, and Coherent Corp are all investing heavily in optical networking technologies tied to AI infrastructure.

Nevertheless, the sheer scale of expected demand growth may allow multiple winners to coexist.

Final Investment Thesis

Lumentum has become one of the most important yet underappreciated companies in the AI infrastructure ecosystem.

The market is beginning to realize that scaling artificial intelligence is not simply about adding more GPUs. It also requires a massive upgrade to the networking fabric connecting those systems together. Optical connectivity has moved from a supporting technology to a mission-critical bottleneck.

That shift is fundamentally transforming Lumentum’s business.

The company now sits at the intersection of several powerful secular trends:

- hyperscale AI infrastructure expansion,

- optical networking adoption,

- co-packaged optics,

- photonic integration,

- and passive institutional inflows through major index inclusion.

Few companies possess the technical expertise, manufacturing capabilities, and strategic positioning necessary to compete effectively at this layer of the AI stack.

The stock’s extraordinary rally reflects that reality.

However, investors should also recognize that Lumentum is transitioning from a relatively obscure photonics company into a widely recognized AI infrastructure name. That transition naturally brings higher expectations, greater volatility, and more intense scrutiny.

For long-term investors who believe AI infrastructure spending will continue compounding over the next decade, Lumentum increasingly appears positioned as one of the core “picks-and-shovels” beneficiaries of the AI era.

In many ways, the market may still be underestimating just how important photonics will become in the future of artificial intelligence.

FAQ Section

What does Lumentum do?

Lumentum manufactures optical components and lasers used in high-speed data transmission for AI data centers.

Why is Lumentum important for AI?

AI requires massive data transfer between GPUs, which depends on optical networking solutions.

Who are Lumentum’s competitors?

Key competitors include Coherent, Fabrinet, Broadcom, and Marvell.

What is the biggest risk for Lumentum?

Customer concentration and supply chain constraints.

Is Lumentum overvalued?

It trades at high multiples, making it sensitive to expectations and market sentiment.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any financial decisions. We are not responsible for any investment losses incurred based on the information provided in this article.